Most acquisitions fail. Yet a few serial acquirers have created immense value for shareholders. What makes the difference? Can we separate the good deals from the bad eggs before they are announced? Let’s take a look at a live example.

Pushpay’s Profit Inflection Point

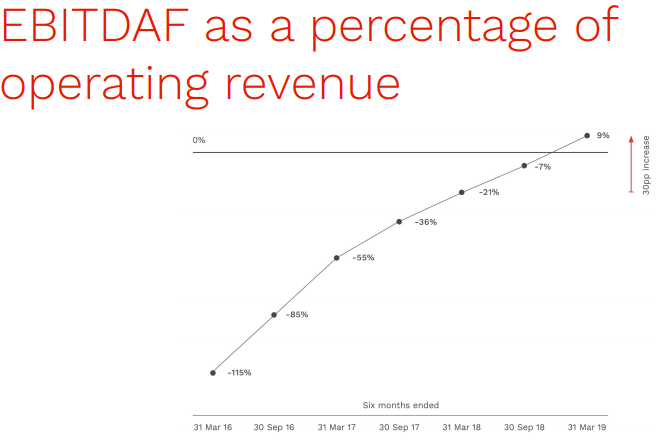

Pushpay tipped passed a fundamental inflection point earlier this year as the business scaled in to cash flow positive territory. The market’s reaction has been positive: the shares are up 43% from their December lows. Most of the Church giving software provider’s operating costs are fixed, so when revenue continues to grow from here, Pushpay is set to gush cash.

Pushpay gave operating profit (EBITDAF) guidance for the first time this year. Last week the company upgraded that guidance further to be between US$18.5 to US$20.5 million. Not bad considering that we are only three months into Pushpay’s financial year.

Pushpay has signaled that they will be using these cash flows to fund the acquisition of other software businesses in the faith sector. The platform is now at scale, so any incremental revenue Pushpay can add will fall to the bottom line faster than one of Scrooge McDuck’s money bags.

At Pushpay’s AGM earlier this week, the company’s new CEO Bruce Gordon, noted that the company is looking at several potential acquisitions that could add to Pushpay’s product suite and scale. Australasian banks have indicated they will be comfortable lending up to 3 times Pushpay’s EBITDA, which indicates a potential acquisition war-chest of US$60 million. Pushpay also has a few options to increase their firepower such as issuing the vendors with shares based on how the acquisition performs after purchase.

The Art of the Deal

News that a company is about to start making acquisitions should be taken with caution for one simple reason: most acquisitions fail.

Cultures clash, synergies no-show, and shareholder value is squandered. McKinsey found that only 17% of mergers deliver the revenue synergies that management were forecasting at the time of the deal. Meanwhile a KPMG study found that over 80% of mergers and acquisitions fail to create shareholder value. Those are rough odds. Statistically speaking, you’d get a fairer shake from a spin of your local pokie machine.

But acquisitions can be extremely successful. One of the best performing companies in the world has been built on a virtuous cycle of continuous acquisitions. Constellation Software’s shares are up 3,700% over the past 10 years alone, thanks to a smart, disciplined, and well-executed acquisition strategy.

So what separates the good deals from the bad eggs? Super-achieving acquisitions tend to share a few common traits. Typically the target company:

- Has an employee culture that matches the acquirer (or can be successfully operated in a completely separate silo).

- Delivers a new technology/product to the acquirer that saves development time, or adds scale.

- Has sticky customer relationships with high switching costs (so that the newly acquired customers don’t run away if there are any stumbles).

- Has genuine revenue and cost synergies with the acquirer.

- Provides a new competency or other strategic value.

- Is available at an attractive valuation.

That last point, valuation, is always the most important. Choosing the right target company matters a lot, but paying too much can turn even the sweetest milkshake sour.

So let’s review six of the company’s most likely acquisition options.

Option 1: The worst deal

The worst possible option in my view would be to purchase a business from Ministry Brands.

Ministry Brands is a private-equity backed holding company that has rapidly acquired a collection of 31 different faith-based software companies over the past few years. Ministry Brands is big. It reports to have 55,000 church customers and in 2017 generated over $100 million in EBITDA. That size is the result of an aggressive slash-and-burn acquisition strategy that is straight out of the private equity playbook. Ministry Brands buys a software company, cuts staff numbers to the bone, reduces investment, strips out any costs it can, and raises prices for customers.

That is never a beloved business model, and is particularly despised in the principles-driven faith-based software sector. Ministry Brands has a poor reputation with churches, and rock-bottom staff satisfaction. The approach is so disliked that some church software companies now publicly reassure clients that they are ‘not for sale’.

The private equity company that owns Ministry Brands is now looking for potential buyers, so the whole collection is potentially up for grabs. The entire package would be too big for Pushpay to purchase outright (excluding some insanely leveraged deal). However Pushpay could be tempted to purchase one or two of the 31 software companies that form part of the collection.

This would be the simplest deal to get done, since Ministry Brands is both experienced at these types of transactions and is a willing seller. But it would likely be a bad move. Pushpay would be buying from a sophisticated private-equity seller that has already done everything legally possible to squeeze all the juice out of the lemon before they sell it. It’s possible that there are some gems hiding in the dirt, and any asset can become attractive at a low enough price. But this deal should come with a big ‘Buyer Beware’ sticker. Avoid.

Deal rating: 3 out of 10

Option 2: Tackle the Innovator’s Dilemma

For many years Pushpay had a broad brush, signing up churches of all shapes and sizes. But in mid 2017 the company narrowed its approach, restricting its sales efforts to what it termed ‘Medium and Large’ sized churches. Medium churches are defined as those with over 200 weekly attendees, while large churches are those with 1,100 or more. The largest U.S. churches can have over 40,000+ weekly attendees.

This shift was probably the right call. At the time Pushpay was still in heavy cash-burn mode, and its internal analysis found that larger churches were vastly more profitable. These customers had bigger budgets, so could afford to pay more for Pushpay’s software, and generated higher payment processing fees. The bigger churches also tended to fully implement Pushpay’s giving solutions and admin platform, and so they had much higher retention rates. Pushpay calculated that small church revenue retention rates were just 80%, compared to over 100% for large churches.

Lastly, the weekly attendance of the largest ‘mega-churches’ has been growing fast as younger people prefer the energy and scale of a bigger church. That growth has come at the expense of the smallest churches, which typically see their weekly attendance slowly decline. Roll it all together and the large church segment is vastly more attractive for Pushpay.

So Pushpay stopped selling to small churches and focused their energy exclusively on larger clients. This allowed Pushpay to get to profitability faster, as has been demonstrated in the latest results.

But by doing so, Pushpay opened the door for a lower-cost competitor to target this small-church customer segment. This presents Pushpay with a potential Innovator’s Dilemma: when a small competitor is able to challenge a much larger incumbent by offering a lower-cost product. Initially the low-cost product is inferior, but over time, and with enough scale, the new upstart can sometimes challenge the incumbent on quality too. When a low-cost competitor can also sell a high-quality product, it’s often game over (just ask any business that has tried to take on Amazon head-on).

Enter Tithe.ly. Founded by a former pastor, Tithe.ly has a similar modern digital approach to donations management as Pushpay. I have been monitoring the company since 2016, and for many years Tithe.ly was not a concern. It was sub-scale and severely under-funded. The company’s low prices and small church clients meant that it could not afford to invest in sales, product, systems, or customer support on nearly the same scale as Pushpay. Tithe.ly had not raised meaningful capital, and as of April 2017 was processing just ‘tens of millions’ of dollars in donations, compared to the billions that Pushpay was processing each year.

Pushpay’s exit from the small church segment changed all that. Pushpay’s sales machine was no longer targeting the small churches, which allowed Tithe.ly to hoover up thousands of these customers over the following years. Tithe.ly has used this new found momentum to raise meaningful capital, starting with two US$2m funding rounds in 2017 and 2018. Then in March of this year Tithe.ly raised a USD$15 million funding round, which valued the company at USD$129 million. Tithe.ly plans to use the cash to hire up to 30 more engineers over the next year to build out its platform.

Today Tithe.ly counts over 10,500 churches as customers and is reportedly growing fast. These small church customers are significantly less valuable than Pushpay’s, so in total giving and revenue terms Pushpay is still many multiples larger. But the recent funding round, and the potential for Tithe.ly to disrupt from the low end, makes it a very credible threat to watch.

Pushpay could respond to this threat in a few ways. It could continue to focus its energy on robustly defending the Medium and Large church segment. If Pushpay can make its product sticky enough, it may be able to avoid low-end disruption altogether. Some of the other acquisition options we will talk about later can help this.

Alternatively, Pushpay could launch its own low-cost brand. Airlines have been using this strategy for years (think Qantas and Jetstar) with mixed success. This has the advantage of being cheaper, but could easily distract management.

An even bolder move would be to acquire Tithe.ly outright. But given the culture clash of premium Pushpay and low-cost Tithe.ly, the acquisition would likely flop unless they were able to run the two businesses independently. Also the tech startup scene is frothy, so Tithe.ly’s valuation may already be outside Pushpay’s budget.

This deal would have the potential to solve a major long-term challenge, but it would come with a lot of risk. Whether it is by acquisition, or other means, Pushpay need to be taking this Innovator’s Dilemma threat seriously. One to watch.

Deal rating: 6 out of 10

Option 3 – Go vertical: Buy a Church Management System

At the core of every large church is a Church management system or ChMS. These are similar to an enterprise resource planning system. A ChMS allows the church to do everything from manage their services, keep track of child check-ins, and roster volunteers. It’s an integral system of record, with very high switching costs.

Pushpay’s giving solutions integrate with numerous ChMS’s. Until now, Pushpay has avoided offering its own ChMS so that it is not competing with its own distribution channel. But as the market has matured it has become more common for payments providers to do both.

There are numerous potential ChMS’s that Pushpay could acquire. Church Community Builder (CCB) is a ChMS that Pushpay has had a longstanding relationship with, and which serves over 4,000 church clients. However CCB’s software stack is outdated and generally not up to the premium quality of the rest of Pushpay’s products. The move here would be to acquire the business primarily for the sticky customer relationships. Pushpay could cross-sell its giving product to those CCB customers that don’t already have it, and then modernise the software itself over time.

Another approach could be to buy a ChMS which is smaller but has more modern tech. The software would be up to Pushpay’s standard much more quickly, but with the trade off that there are fewer customers on day one.

The dream purchase in my view would be a ChMS like Planning Center which is growing fast, has over 50,000 church customers, and a very clean and modern user interface. Planning Center has no sales team, it reinvests all its cash in to product development. Planning Center’s product is modular with nine different products that can be sold individually. This makes it a great complement to Pushpay who could let their formidable sales team loose with a high-quality product suite. It does raise the risk of a culture-clash, but given the other strategic similarities this may not be such a big deal. Unfortunately Ministry Brand’s slash and burn approach to acquisitions has led Planning Center to publicly declare to clients that it is “not for sale” so it may be tough for Pushpay to win over the founders.

In any case, acquiring a ChMS would significantly deepen Pushpay’s relationship with its customers, boosting retention rates and increasing switching costs. It would also give Pushpay the opportunity to market a new product to its existing clients.

Overall it’s a solid acquisition opportunity. But I would caution against purchasing a sub-standard technology product with the plan to improve it. When a team of developers need to constantly patch over holes in a leaking ship, it can be tough to take the time to build a new, modern software product.

Deal rating: 7 out of 10 [Add one point if Pushpay buys a modern ChMS, add two points if they somehow pull off acquiring Planning Center]

Option 4: Buy a competing Engagement App

Pushpay is more than just a payments processor, it also provides churches with ‘systems of engagement’. In other words, apps for churches. These apps become core to the church’s interaction with their members. The attendees can watch past sermons, follow along with bible verses, and register to attend a particular session. Most importantly for Pushpay, these apps also integrate a giving button which then allows a user to make a one-off or recurring donation.

That last feature is key. Most church app providers make the vast majority of their revenue from providing the software. Pushpay charges for the app software, but generates most of its profits from the donation processing fees. This leads to some sweet alignment as Pushpay is incentivised to maximise both engagement with the app, and total giving. Churches win because they receive greater donations, and Pushpay wins by receiving a cut of the increased processing volumes.

There are two main competitors that Pushpay could look to acquire here, Subsplash and Aware3. These companies are both currently the app providers for thousands of church customers. However neither are meaningful players in donation processing. That means that the customers of both Subsplash and Aware3 are more valuable to Pushpay than they would be to the companies themselves. That’s an attractive feature when making an acquisition. Pushpay could acquire either business, and use it’s more advanced sales team to cross-sell their giving solution to thousands more churches.

One wrinkle is that both Aware3 and Subsplash have been trying to emulate Pushpay’s donation processing business model (without significant success), so they may be reluctant to sell out and give up on the big prize for themselves. Also Subsplash and Pushpay have battled aggressively in the past in their marketing, so there is the risk of a culture-clash if Subsplash is acquired.

If Pushpay are looking for a safe bet for their first major acquisition, the purchase of Aware3 would be a leading candidate.

Deal rating: 7 out of 10

Option 5: Buy a Catholic software product

To date, almost all of Pushpay’s customers have been evangelical and Protestant Christians. That leaves a very large denomination where Pushpay has yet to gain traction: the Catholic Church.

Catholic churches are large, with just 20,000 churches serving 59 million attendees (that’s around 3,000 attendees per church). That should be a good fit for Pushpay’s product. But the Catholic church tends to be slower to adopt new technology. It is also more hierarchical in its decision making. One high level decision can see a certain software solution adopted by an entire region. That makes any new deal harder to win, but potentially much more valuable.

By acquiring an existing Catholic software company, Pushpay would gain a foot in the door. It could then leverage that existing trusted relationship to demonstrate its full suite of giving and engagement products. It won’t be an automatic win, but the potential is big enough that it is worth serious consideration.

Deal rating: 7.5 out of 10

Option 6: Buy an adjacent product

Pushpay currently has two products: giving and engagement (apps). It is also working on its own donor management module so that it can deepen the relationship with its customers. But there is a big church software world out there with many other new products that Pushpay could develop or acquire.

A strong acquisition for Pushpay would be to buy a fast-growing small software company that provides one of these adjacent products. For example Brushfire provides an events management and ticketing product that helps churches manage events outside of their usual weekly service. The product itself doesn’t have the incredible unit economics of Pushpay’s giving solution, but it would make Pushpay’s customers even more likely to stick around. It would also provide a new product that Pushpay’s sales team could sell to their existing customers, and earn some high-margin incremental revenue for their trouble.

There are many products like this that Pushpay could acquire, significantly reducing their time to market. These companies would likely be well within Pushpay’s budget, add a lot of strategic value, and are likely to be a good cultural fit.

Deal rating: 8 out of 10

Pushpay’s Next Adventure

Pushpay has tipped past a fundamental inflection point, and its strong operating leverage means the business is set to gush cash. Pushpay can now put that cash to work on some smart acquisitions. The core platform has reached scale, so any new high-margin revenue will generate additional free cash flow. That could enable further acquisitions and accelerate the value-creation flywheel.

Pushpay will need to avoid the traps, and find a business that fits both strategically and culturally. Most importantly in this frothy market, Pushpay will need to maintain valuation discipline and pay a reasonable price. If it can do all that, a smart value-creating acquisition could be a match made in heaven.

Subscribe to receive an email when a new update is released:

Disclosure: At the time of publishing Matt has a position in Pushpay. Holdings are subject to change at any time. This report, and disclosure, should not be considered to be a recommendation.

Thanks Matt, it’s obvious from this deep-dive that you’ve been doing your research. I’ haven’t yet read a more detailed summary of Pushpay’s growth options. Good to hear from you again.

Thanks Tim! It’s a longer post than usual but I’m confident that folks that read to the bottom will have a better handle on Pushpay’s acquisition options than 99% of the market.

Excellent post.

Thanks Kristian!

Hopefully Pushpay’s board read this article. Maybe you could consult for them. Great research Matt, thank you!

Thanks Harry! Much appreciated.

Thank you for answering many of the questions that had been in my thinking since I added them to my portfolio. Excited to see what the future holds! Was also sad to see Three Wise Monkeys podcast finish, just as an FYI!

Thanks Ben. Pushpay still has a few challenges to work through as I outlined, but there is the potential for some smart deals.

Nice in depth, well-researched article Matt. Good to hear from you again. I was getting a bit doubtful about Pushpay as they seemed to be going nowhere, but you have restored my faith!

Thanks Brian! Pushpay has a lot of its future growth baked in now after the recent run up in share price. But I will be watching their next acquisition closely. Glad you enjoyed the article!

Hi Matt,

You talk of acquisition experts and WTC comes to mind as their whole strategy seems to be heavily acquisition biased. Indeed, from their record they seem to be very successful- do you have any thoughts on what could be described as an excellent extreme example. Disc: I own shares in WTC and PPH

It’s hard to go past Constellation Software which I mention in the article. It is a really outstanding example. The tech giants in the U.S. are all serial acquirers too, its just not as obvious because their core business is also growing so fast. I think software businesses lend themselves to being good acquisition targets as they tend to match a lot of the criteria of good acquisitions (high switching costs, unique assets etc.)

OK thanks Matt. As you say, if they get it right it works – as with any strategy of course – but this one seems to be a particular success with software companies.

Great article Matt. I have been following you for some years in your previous work life and like many am waiting for you to start up a similar service for the believers. Cheers

Thanks Henry!

Another indepth article Matt. This is the sort of detail investors are looking for, things can change quickly and you are ahead of the game here. Many thanks for sharing.

Thanks Unclewally! Glad you enjoyed the update.

Matt, the depth of knowledge and understanding of the sector you have shown, is a great example to us all. Many thanks for thsi great insight into the sector.

Thank you Sean. You are a very thoughtful investor yourself so it is doubly appreciated. Glad you enjoyed it.

Thanks for sharing the great content Matt. Very lucky to get your insights. Look forward to your next article.

Thanks Froxy!

Hi Matt. You demonstrate a very thorough knowledge of Pushpay’s industry. When Pushpay does start making acquisitions you will be in a great position to analyse them ahead of most other people.

Thank you John. I am a big believer that fortune favours the prepared mind. Glad that you enjoyed the article!

Thanks for the write-up Matt, very insightful.

Thanks Graham! Glad you enjoyed!

Love the work and thought you have put into this we miss the three wise monkeys podcasts a lot!

Glad you enjoyed it, thanks Ritchie!

Hi Matt, curious what your thoughts are on the recent SP weakness?

Hi Froxy, I missed your comment earlier. I don’t have any comments on share price swings, and as noted above, covering Pushpay’s potential acquisition options shouldn’t be read as a recommendation. The business itself is ticking along, growing more slowly, but more profitably, than it did previously.

Matt, I enjoyed this in depth analysis of strategic options,… I hope the PPH management team read it too. For the reasons you state, I am always nervous when material acquisition becomes part of a company strategy. I still hold PPH from your PRO recc, and I hope they will allow the time and transparency for investors to see how the CCB acquisition and integration tracks.

Thanks Michael, glad you enjoyed the update! I can see that a lot of people in the industry both at Pushpay and its competitors have read this particular article.

May God bless you.