Over the past 22 years, the shares of Monster Beverage (NASDAQ:MNST) — best known for its large cans of Monster brand energy drinks — increased in value by a mind-numbing 2,300-fold. That is almost too big of a number to wrap our heads around, so let’s put it like this: for every $10,000 invested in 1997, a shareholder that held on would be sitting on $23,200,000 today.

In 1997 that $10,000 could have bought a decent second-hand car. Today, after investing in Monster Beverage it would buy them a helicopter to go with their cliff-top mansion.

Monster Beverage is one of my favourite investment stories of the last few decades. It’s not just because of the spectacular returns. It’s because it was an easily understood business, and at several points in its journey, clearly undervalued. Monster Beverage demonstrates a particular path to massive wealth creation for shareholders. A path that doesn’t require lucky flukes, or taking huge risks.

Monsters

While most of the market is mired in mediocrity, there is a small group of companies that generate insane returns for shareholders. I call these companies Monsters for the way they dominate their industries and transform portfolios. A few years ago I set out to study these huge monster winners, reading books like ‘100 to 1 in the Stock Market‘ and trawling through Standard & Poors data to see if I could identify any common traits. Most importantly, I wanted to see if it was possible to identify these winners early, before they started their huge run, and the rest of the market caught on.

The Four Steps

As I see it, there are four steps to catching a Monster:

- Choose your hunting ground – avoid pretenders to the Monster throne.

- Catch your monster – identify key traits.

- Watch closely – continuously monitor and sell quickly if your thesis is broken.

- Hold on – be able to stomach the volatility without selling too early.

I’ll talk through each step in turn.

Choose your Hunting Ground

Investing is an art of negative space. What you don’t buy is at least as important as what you do. The best investors say no to potential ideas early and often.

The vast majority of companies have no shot at generating monstrous returns. These businesses should be avoided entirely. They are either struggling to keep the lights on, or they have already begun their long descent into obscurity. If you buy mediocre businesses you’re not going to be able to capture the kind of returns we are seeking.

But there are also four other types of companies that can generate big returns, that I don’t count as Monsters. These are companies that rely on luck or high risk. And for that reason, even though they can deliver high returns, I still avoid them:

Lucky speculations

If these companies had a motto, it would be: ‘it’s better to be lucky than good’. There is nothing wrong with being lucky, but it’s not a repeatable strategy. Winning the lottery 5 times in row is pretty rare.

Speculative mining companies are the archetypal example. Every now and then some bonfire for shareholder capital actually manages to strike oil/gold/lithium and hits the big time. There’s a reason Australia is called the Lucky Country, and there are plenty of these stories around. The problem is that there are several hundred speculative miners on the ASX. The vast majority of these businesses are cash-infernos. Accurately forecasting winners in that space is almost impossible.

Speculative biotech and pharmaceutical research companies are a similar breed. At least they are attempting to do something more useful than put holes in the ground. But good intentions don’t equal a good investment.

I avoid these speculative ‘lotto tickets’ entirely. Good luck to all players. Not my game.

Commodity price swings

These are companies that soar due to a sharp change in the supply-demand ratio for a basic commodity. The commodity price rockets, taking the company’s shares with it.

This tempts many otherwise smart investors: use your big brain to identify some commodity that will be in high demand, and buy the producers of that commodity before the price rises. In practice, it is extremely difficult to forecast these commodity price swings, and even harder to profit from them. Increased demand typically brings in legions of new suppliers, which ultimately send prices crashing back to earth faster than a lump of unwanted coal.

If you think you can forecast commodity prices well enough to pull this off reliably, you should probably be day-trading commodity futures. Good luck with that.

Highly-leveraged businesses

Companies which have a huge amount of debt can have some interesting properties. If the debt is large enough, and the business manages to avoid being crushed under its own weight, it acts as a big amplifier of returns, good or bad.

The math of leverage explains why. If a business has total debt of $90m, and a market cap of $10m, we would say it has an enterprise value of $100m. If the business doubles in value to $200m, this extra $100m of value would all go to the equity i.e. to shareholders. So a 100% increase in business value results in the company’s market cap increasing ten fold to $100m, and the shares soaring 1,000%.

On the other hand, if the business’ value falls by even 10%…

These highly leveraged companies can be very profitable for shareholders, but the leverage is a double-edged sword. If things don’t work out these companies’ share prices face a large ‘crash risk’, and the sword stabs its owner in the leg. The debt can even overwhelm the company and push them in to bankruptcy.

I like my thai food spicy, but not my shares. Pass.

Back from the brink of bankruptcy

These are zombie companies that were once on death’s door and have now re-entered the land of the living. Buying companies that are going through a panic, or financial distress, can be a winning strategy if the business makes it out the other side.

In times of significant market panic even great companies can be priced like they are going out of business. That would get my attention. But generally speaking, I will leave the zombie wars to others.

That’s four categories I avoid, now let’s talk about true Monsters.

Catch Your Monster

Monsters are businesses that deliver huge shareholder returns by compounding high returns on invested capital. These businesses generate strong free cash flows, and most importantly, the business is able to reinvest those cash flows at high rates, and for a very long time. That reinvestment has a compounding effect over time, with the company’s value building up faster than a snowball rolling downhill.

Altium, Appen, a2 Milk etc. all fall into this camp. I have found there are four key traits these monsters tend to have at the start of their journeys:

#1: They start out small

This might be an obvious one, but it’s important. It is much easier for a company to increase in value 100-fold or more, if it is starting from a low base. Today Amazon is valued at $900 billion. The shares are up 1,200x because the company started off small. For Amazon to increase another 1,200x from here would give it a market cap of over 1 quadrillion dollars. That’s a sum so large it is greater than the value of every financial asset on earth. Jeff Bezos has some ambitions for Space exploration so perhaps we shouldn’t write it off. But it is safe to say that growing gets tougher the bigger you are.

This is why I focus on fast-growing small companies with long growth-runways ahead.

#2: Unique edge

The company must have some kind of durable competitive advantage that forms a barrier to competition. This barrier allows the company to earn those high returns on invested capital, and to ensure that those returns are not eroded over time by new competitors.

These advantages can come in many forms. They include consumer brands, patents, intellectual property, switching costs, economies of scale etc. The most powerful edge usually comes when a company combines both demand advantages and supply advantages. The very best businesses are then able to link these two edges together in a positive feedback loop or ‘flywheel effect’.

My goal is to identify companies with these competitive advantages, and where the advantages are increasing over time.

#3: Superior Management

The importance of high quality management is magnified in a small fast-growing company. If the captain of a large ocean liner steers the boat off course, it takes a long time for the effects to be felt. But if a small speed-boat captain turns the wrong way, they can quickly find themselves on the rocks.

We need a management team that thinks long-term, and has the vision to understand their competitive playing field. This is why we focus on identifying high-quality and aligned management teams. Ideally the founders are still in charge, or management at least hold a large number of shares and behave like owners.

Assessing management is so important to my process that it is very rare that I haven’t met with a management team before buying shares, and often I meet with them several times before becoming comfortable enough to initiate a position.

#4: Misunderstood

I left this for last because it is the most important. There is no business so beautiful that it can’t become an ugly investment at the wrong price.

To achieve truly spectacular returns, a company has to start off with a valuation that does not fully reflect its market-thumping future. Ideally it will begin its journey with a valuation that is downright cheap, and then the market’s rising expectations will add a multiplier effect to its growth.

Ultimately the most important step in determining whether to add a potential Monster to the portfolio is to assess its intrinsic value and then to buy at a significant discount to that valuation. And to be undervalued is to be misunderstood.

Whenever we are deciding to buy a business we are asking ourselves what our variant perception is compared to the market. What do we believe that the market disagrees with us on? Perhaps the market doesn’t think that growth will stick around for as long as we do. Maybe it’s not giving credit for new products or geographies. Whatever the reason, their mistake is our potential to profit.

Buying companies at a discount to their intrinsic value is at the core of all sensible long-term investing, Monster-hunting is no different.

Watch closely

The price of catching monsters is eternal vigilance.

Once you have caught your monster, the next step is to clearly articulate your thesis at the time of purchase and then regularly review that thesis as new information comes to hand. Actually writing out your thesis is important.

Not every company that I thought had Monster potential actually delivered. So a core part of my strategy has been to sell quickly when my investment thesis has been invalidated. Class Software is the clearest example of being willing to cut bait quickly when a thesis is broken, as I covered in detail in The Selling Blindspot.

Hold on tight

Catching Monsters takes patience. But even more than that, it requires conviction.

Holding on to a company is much tougher than just passively waiting for the cheques to come in. It means enduring the pain of seeing your company’s share price fall and fall, and maintaining the conviction that it will come out the other side stronger. There is a critical tension here between holding on and selling quickly. The deciding factor is your investment thesis. If it is intact, hold on and ignore the market’s price swings. If the business’s quality is eroding, be prepared to sell quickly.

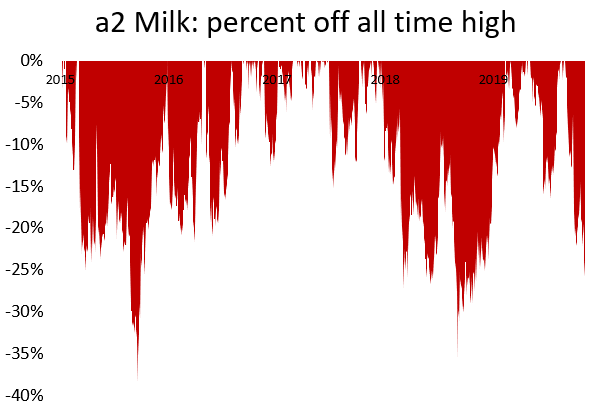

This is what I like to call a ‘pain chart’, inspired by a Morgan Housel article, for a2 Milk. This chart shows when, and by how much, a2 Milk shares were below their all-time high. (Periods at 0% show when shares hit a new all-time high). Remember, this was during a period when shares increased more than 1,600%:

There have been five times when a2 Milk’s share price fell 20% or more. And on two occasions the shares fell by 30% or more. To enjoy the monstrous gains to date shareholders needed to avoid giving in to fear and selling during those troughs of despair. Those shareholders also needed to avoid the temptation to lock in a profit when the shares were up 30%, 100%, 500%, or even 1,000%.

To hold for that wild ride, investors need to develop, and maintain, a high level of conviction that their investment thesis is correct. Then, ultimately, they need to be proven right.

Most of the market is incredibly short-term oriented. This applies to individual traders as well as large fund managers. These investors are always trying to own the hottest-stock-this-quarter while missing the 100x Monster that is growing beneath their feet.

If you can tune out the market’s noise you will separate yourself from the others.

Vision, Courage, Patience

Catching Monsters is hard. Our view of the future is cloudy at best. The power of compounding means that the biggest winners will create most of their value many years, or even decades, from today. Forecasting that far in to the future is not easy.

Investors need the imagination to be able to think big. To visualise how the company could be performing in the distant future. But then they also need the discipline to bring that big vision back to the reality of the present day, and value it appropriately. That marriage between lofty big picture thinking, and the cold hard facts of present day valuation, is tougher than it sounds.

“To make money in stocks you must have ‘the vision to see them, the courage to buy them and the patience to hold them’. Patience is the rarest of the three.”

100 to 1 in the Stock Market author Thomas Phelps expanding on a quote from financier George F. Baker.

If you can demonstrate those three qualities: vision, courage, and patience, you have a shot at aligning your portfolio with these unstoppable engines of wealth creation. The ride can be bumpy, but it’s also a heck of a lot of fun.

Subscribe to receive an email when a new update is released:

Disclosure: No part of this report, or disclosure, should be considered to be a recommendation or financial advice. At the time of publishing, Matt holds shares in a2 Milk. Holdings are subject to change at any time.

Hi Matt, please keep me up to date with the new venture. Henry Adams ( John McKay)

Thanks Henry, will do!

Can’t wait to see what the new project is Matt. Really enjoy all your writing, missing the 3 wise monkeys podcast and you’ve been truely missed since you left pro.

Thanks Turns! Watch this space!

Love the post. We must compare our baby monster nurseries sometime. regards, Sean

Thanks Sean! Sounds like a plan!

Thanks for the post Matt. I’m also missing the podcasts, and of course your presence at Pro. I can’t wait to hear what the next chapter is all about. I will definitely watching this space.

Thanks Holli!

Awesome post Matt. Been missing the wisdom of the Monkeys. Looking forward to joining your next Fellowship….

Cheers Gandalf!

Hi Matt,

Another great piece! Love your work. You’ve baited the hook well for what’s next!

Is there a risk with catching a baby monster that it could be more vulnerable to a black swan event, if it comes at the wrong time, because they are growing so fast? Possibly intrinsic in some of these small, rapidly growing companies is that they are more exposed to externalities like a GFC that see access to much needed capital dry up, for example? Or their potential customers purchasing patterns change to due a recession? And therefore they find it harder to grow into their multiples.

Or is it actually more likely that baby monsters are more resilient to such events? Because they do have better management, a wider moat, and a stronger business model?

I just wondering what happens if the current market, which still seems to be a bull market even if it is more pessimistic and volatile than it was, ends with more of a bang than a whimper?

Thanks very much Karl, great to hear your enjoyed it, and you’ve asked an excellent question.

Generally speaking in my view baby monsters are more resilient to outside economic forces than the average company for all the reasons you outline. Also because they are typically benefiting from a long-term secular demand trend i.e. from growth of a new product or industry that continues regardless of the economic cycle. Remember we are weeding out companies that are growing due to commodity price swings, and those that are rebounding with crushing loads of debt.

A great example during the last recession was Apple. The GFC was the worst recession in America since the Great Depression, and yet there was still huge lines for every new iPhone iteration. That demand was resilient regardless of rising unemployment and reduced overall household spending. Our mission is to find those type of companies which can grow in all seasons. Most of the Monsters we are looking for fall in to that category.

You are quite right though that baby Monsters can be burning capital at various points of their growth cycle. Part of our role as portfolio managers is to balance risk exposures. At this point in the cycle I am limiting my allocation to companies that are dependent on raising more capital. And even for those that are in cash-burn-mode, I will give a greater weight to companies that could self-fund their growth if they took their foot off the accelerator. For many years Xero was a great example of this, they were burning capital, but if they stopped spending on marketing, they would be profitable very quickly. Similarly if a company is dependent on one-off capital sales (compared with recurring/repeating revenue) that will earn it a smaller spot in our portfolio.

All of this is not to say that the share prices of high-growth, high-quality companies won’t fall during an economic slow down, they almost certainly will. Some ‘darlings’ will be hit hard. But the great businesses themselves will be intact, and many will bounce back stronger. Some will even pick off weaker rivals while they are struggling. The key is doing the hard work to develop a well-held conviction in the underlying fundamentals.

The challenge in the meantime is to maintain valuation discipline and focus. I didn’t touch on position sizing in this article but just like when I was managing capital professionally, I have trimmed position sizes for all of the companies mentioned, when their valuations ran ahead of the fundamentals. That capital is then recycled in to higher conviction smaller companies that are earlier in the journey. Ultimately we should only be buying/holding companies at a given price if we think it’s an attractive deal. We should be happy for the stock market to close and only reopen in several years time.

The price of Monster hunting is eternal vigilance, and that applies to portfolio management too. But that is a topic for another update! Thanks again for the great question Karl.

Great post Matt, interesting concept, although I think it takes a long time to know if you got it right or got lucky – from my perspective two of those potential monstors are businesses I was unable to develop any conviction regarding their investibility, A2M & Nearmap. I amy turn out to be very wrong!

Thanks Ricky. Glad you enjoyed it, and thanks for the comment.

Separating luck vs. skill is a big part of why investing is so challenging. I’d like to do another update in future to unpack the different types of luck. The ‘lucky speculations’ that we are not seeking are commonly described as ‘blind luck’ or ‘dumb luck’. This is the type of luck where the odds were extremely poor when you place your bet, and yet you win. Buying a lotto ticket for example has significantly negative expected value, but some people win. That’s fun, but it’s not how we build a portfolio.

There are other kinds of luck that we do try to expose ourselves to. One example is companies that have multiple ways to win, or multiple adjacencies that they can expand in to. If the unforeseen expansion works, I refer to these as ‘windfall luck’. This is where the odds are in your favour to begin with, and then you have an even better outcome than you expected. In poker this would be like betting because you have a flush, and then another card comes out and you have a Royal Flush.

There is also a sentiment component. There are random swings in market sentiment that push stocks up and down. For that reason I find it best to focus on how the fundamentals have performed.

Taking the a2 Milk example, the shares are up around 1,600% since the time of purchase in 2015. That sounds like a lot, but it’s worth remembering how the fundamentals have performed too. Since 2015 the company’s revenue is up 740%, and profit before tax is up 13,800% (albeit from a low base). At time of purchase a2 Milk’s market cap was around $515m. Last year a2 generated $415m of profit before tax, has a $293m shareholding in Synlait, and has $464m of cash on its balance sheet with no debt.

I agree that since the future is inherently probabilistic, we can never know with certainty whether investing in a2 Milk in 2015 was a good decision. But in my view the scale of a2’s fundamental performance indicates that there is a high likelihood that it was.

Ultimately even when we have a bet with the odds on our side, i.e. with positive expected value, it doesn’t mean that an individual investment will have a good outcome. Which is why the best way to measure success is always the performance, over the long-run, and across an entire portfolio. At that level the randomness of luck will balance out across multiple positions and time periods.

Thanks Matt, this is a fabulous article. Very informative.

Can’t wait for your exciting new project. Please make it soon.

I joined Pro only a short time before you left, and while I could see the fabulous stocks you had chosen, I felt that entering many of them at that stage was too risky price-wise. I was right is some cases, wrong in others. But it will be fantastic to be involved from the get-go with a new Matt Joass portfolio or advisory.

All the best,

Ann

EyesWideShut

Very informative and interesting Matt. Count me in please

Thanks Brian!

Pingback: The Bizarre, Weird, and Beautifully Inefficient World of Aussie Small Caps | Matt Joass

Pingback: Hunting For Monsters – Have I Found A Monster In Addus? – Live Hard